Innovation Terms (Glossary)

Mar 09, 2024

By Ari Manor , CEO at ZOOZ

This is one in a series of articles that provide detailed and updated information about Innovation.In this specific article, which focuses on Innovation Terms (Glossary), you can read about:

- Diffusion of Innovations

- Disruptive Innovation

- Entrepreneur

- Innovation Day

- Innovation Fellowship

- Innovation for Automation

- Innovation Fund

- Innovation Hub

- Innovation Lab

- Innovation Leader

- Innovation Network

- Innovation to Zero

- Innovation Value

- Innovation without Limits

- Intellectual Properties (IP)

- Radical Innovation

- Thinking Tools

- Innovation Glossary (200 additional terms)

For additional articles about Innovation, see the Topic Menu.

Diffusion of Innovations

The diffusion of innovations theory, proposed by Everett Rogers in 1962, explores how new ideas, products, and technologies spread through society over time. It highlights the importance of understanding the factors that influence the adoption and diffusion of innovations, including the characteristics of the innovation itself, the communication channels used to disseminate it, and the social context in which it is introduced.

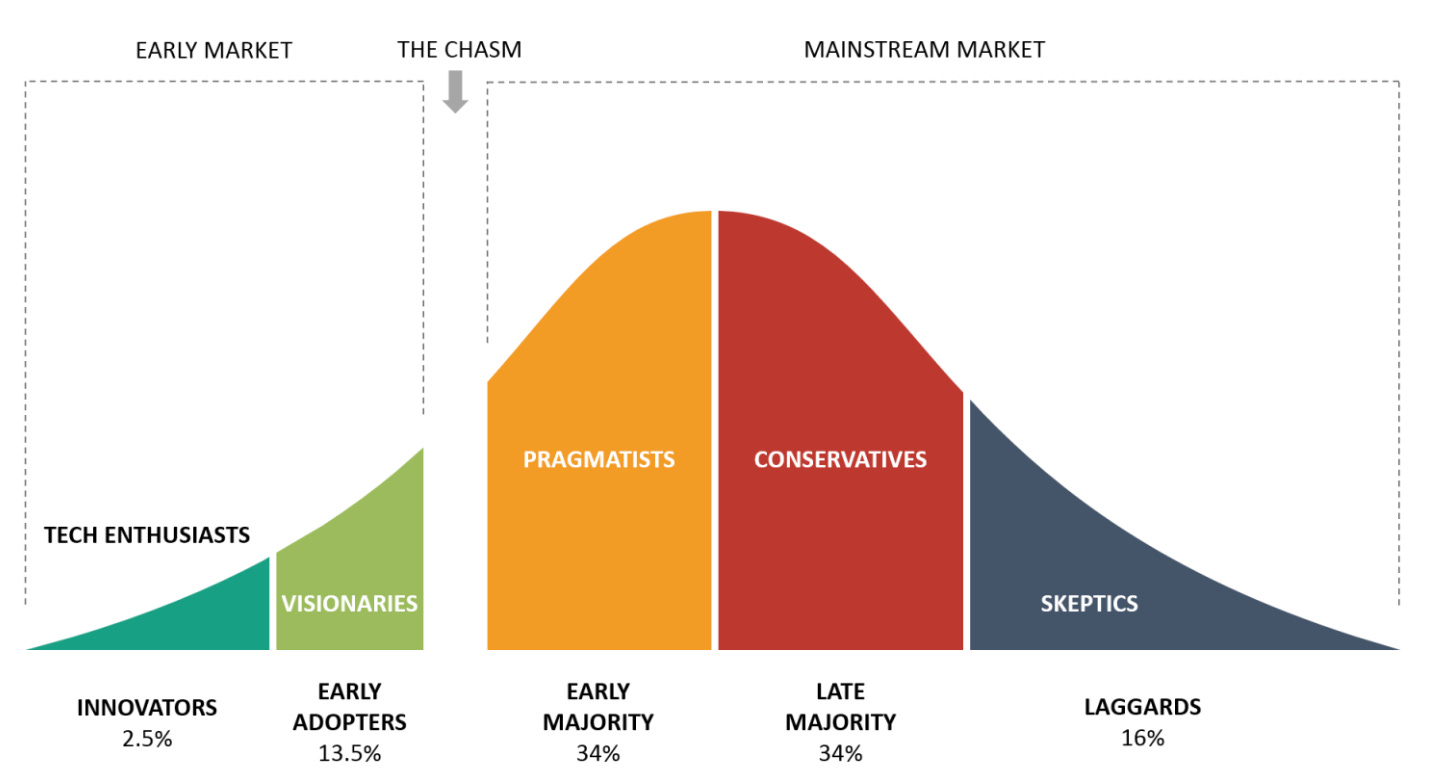

The Adoption Curve

The adoption curve is a pivotal concept within diffusion of innovations theory, outlining the progression of new technologies or practices within a society. Its bell-shaped outline delineates how different societal segments embrace a novel idea, from the earliest enthusiasts to the most hesitant individuals. Understanding this curve is crucial for entities ranging from businesses launching new products to policymakers enacting regulations and those driving social change.

The Adoption Curve Across Different Market Segments

- Innovators (2.5%): These are the first to embrace new concepts, backed by financial resources and a readiness to assume risks. Their initial support is key to an innovation's early validation.

- Early Adopters (13.5%): With their high social standing, these trendsetters offer vital endorsements, thereby confirming the innovation's value to the masses.

- Early Majority (34%): This group is prudent and requires solid proof of an innovation's utility before acceptance, signifying a critical shift toward broad approval.

- Late Majority (34%): Characterized by their caution, members adopt new ideas when they become commonplace, often propelled by fiscal imperatives or social influences.

- Laggards (16%): Traditionally inclined and often of lower socio-economic status, they are the final adopters, driven mainly by necessity.

Grasping the nuances of the adoption curve is essential for anyone involved in innovation. It aids in tailoring marketing approaches, forecasting product life cycles, and allocating resources to ensure an innovation resonates with its target demographic efficiently. For further insights on leveraging the adoption curve to your advantage, read here.

Factors Influencing Diffusion of Innovations

- Innovation Characteristics: Innovations that are perceived as advantageous, compatible with existing values and needs, and relatively simple to understand and use are more likely to be adopted by individuals and organizations. For example, the adoption of electric vehicles (EVs) has been influenced by factors such as their environmental benefits, technological advancements, and government incentives.

- Communication Channels: The channels through which information about innovations is communicated play a crucial role in their diffusion. Traditional channels such as mass media, interpersonal networks, and opinion leaders can significantly impact awareness and adoption rates. For instance, social media platforms like Twitter and LinkedIn have become powerful channels for disseminating information about new products and services to a wide audience.

- Social System Factors: The social context in which innovations are introduced, including cultural norms, social networks, and institutional structures, influences their adoption and diffusion. Innovations that align with prevailing social values, norms, and practices are more likely to gain acceptance and be integrated into society. For example, the widespread adoption of renewable energy technologies like solar panels and wind turbines has been driven by growing awareness of environmental issues and the desire to reduce carbon emissions.

- Time: The rate of diffusion varies depending on the innovation's perceived relative advantage, complexity, and compatibility with existing systems. Some innovations may experience rapid adoption and diffusion, while others may take longer to gain traction and become mainstream. For instance, the adoption of mobile payment technologies like Apple Pay and Google Pay has accelerated in recent years due to increased smartphone penetration and consumer demand for convenient and secure payment options.

- Innovator Characteristics: The characteristics of innovators, including their socioeconomic status, values, and attitudes toward risk-taking, influence their tendency to adopt new innovations and serve as early adopters who influence others' adoption decisions. Innovators are often driven by a desire for novelty, experimentation, and problem-solving, leading them to embrace new ideas and technologies before the broader population.

In summary, the diffusion of innovations theory provides valuable insights into how new ideas, products, and technologies are adopted and spread through society. By understanding the factors that influence diffusion, innovators, marketers, and policymakers can develop more effective strategies for promoting the adoption and acceptance of innovations, ultimately driving positive social change and progress.

Disruptive Innovation

Disruptive innovation, a concept introduced by Clayton Christensen in 1997, refers to the process by which new technologies, products, or services disrupt existing markets and industries by offering simpler, more convenient, and often more affordable alternatives. Disruptive innovations typically start at the low end of the market or serve underserved customer segments before eventually challenging incumbent players and transforming the industry landscape.

Characteristics of Disruptive Innovations

- Lower Cost and Accessibility: Disruptive innovations often offer lower-cost alternatives or serve previously underserved customer segments, making them accessible to a broader audience. For example, ride-hailing services like Uber and Lyft disrupted the taxi industry by offering more affordable and convenient transportation options to consumers.

- Simpler and More Convenient: Disruptive innovations simplify complex processes or technologies, making them more accessible and user-friendly for mainstream consumers. For instance, smartphones disrupted the mobile phone market by combining multiple functions such as calling, messaging, internet browsing, and navigation into a single device, offering greater convenience and versatility.

- Innovative Business Models: Disruptive innovations often introduce innovative business models that challenge traditional industry norms and practices. For instance, the software company Slack demonstrated disruption through its adoption of a freemium model, which significantly altered the landscape of workplace communication tools.

- Note: Unlike traditional software purchases or subscriptions that require upfront payment for the full suite of features, Slack's freemium model allows users to start with a basic version of the software at no cost. This approach lowers the barrier to entry for small teams and organizations, encouraging widespread adoption. As users become ingrained in the platform and demand more advanced features, they are more likely to convert to paid plans. This business model not only facilitated Slack's rapid market penetration but also challenged the conventional sales models of enterprise software by prioritizing user experience and incremental engagement over immediate revenue.

- Focus on Underserved Needs: Disruptive innovations target underserved customer segments or unmet needs within existing markets, offering solutions that address specific pain points or gaps in the market. For example, fintech startups like Robinhood disrupted the financial services industry by offering commission-free trading and easy-to-use investment platforms, appealing to a younger demographic previously overlooked by traditional brokerage firms.

- Incremental Improvement Over Time: Disruptive innovations often start with incremental improvements or niche applications before gradually expanding their capabilities and disrupting larger markets. For example, electric vehicles (EVs) initially faced challenges such as limited range and high costs but have evolved over time to become viable alternatives to traditional gasoline-powered cars, disrupting the automotive industry.

In summary, disruptive innovation is a powerful force that reshapes industries, challenges incumbents, and creates new opportunities for growth and innovation. By understanding the characteristics and dynamics of disruptive innovations, organizations can anticipate market shifts, adapt to changing consumer preferences, and seize opportunities for growth and success in an increasingly competitive business landscape.

Entrepreneur

Entrepreneurs are visionary individuals who identify opportunities, take calculated risks, and create innovative solutions to address unmet needs or challenges in society. As drivers of economic growth and agents of change, entrepreneurs play a vital role in shaping the future by introducing new products, services, and business models that disrupt existing industries and drive progress. Their entrepreneurial spirit and relentless pursuit of innovation fuel innovation ecosystems, inspire others, and create value for customers, investors, and society at large.

Typical entrepreneurship skills include

- Critical Thinking and Problem-Solving: Entrepreneurs must be able to identify and analyze problems effectively and develop innovative solutions. For instance, the founders of Airbnb exemplify critical thinking by reimagining lodging, turning empty spaces in homes into accommodations for travelers.

- Risk Management: Effective entrepreneurs assess and manage risks, not shy away from them. Spanx founder Sara Blakely's investment of her life savings into creating comfortable shapewear is an example of calculated risk-taking.

- Networking: Building a strong network is essential for entrepreneurial success. Reid Hoffman, co-founder of LinkedIn, leveraged his connections to create the world's largest professional network, showcasing the power of strategic networking.

- Adaptability and Flexibility: Entrepreneurs need to adapt to changing markets and customer needs. Netflix’s Reed Hastings shifted from DVD rentals to streaming, demonstrating adaptability in business.

- Leadership and Management: Successful entrepreneurs must lead and manage teams effectively. Mark Zuckerberg's leadership in scaling Facebook from a college network to a global platform highlights the importance of management skills.

- Financial Literacy: Understanding finances is crucial for making informed business decisions Jeff Bezos displayed this skill by strategically reinvesting profits back into Amazon, focusing on long-term growth over immediate profit.

- Marketing and Sales: Entrepreneurs should excel at marketing their products and closing sales. The success of Kylie Jenner's cosmetics line illustrates the impact of strong marketing and sales skills.

- Innovation and Creativity: Constant innovation is key to staying competitive. Elon Musk’s ventures like Tesla and SpaceX underscore the significance of creativity in entrepreneurship.

- Persistence and Resilience: Overcoming setbacks is a vital entrepreneurial skill. Steve Jobs' return to Apple and his subsequent revival of the company into a tech giant exemplifies the resilience needed in entrepreneurship.

- Negotiation: Strong negotiation skills can lead to better deals and opportunities. Oprah Winfrey's ability to negotiate partnerships and contracts has been central to building her media empire.

Entrepreneurs stand at the helm of innovation, their unique blend of vision, courage, and ingenuity propelling society forward. In their relentless pursuit of progress, these trailblazers not only shape industries but also foster the growth of global economies and inspire the spirit of enterprise in others.

Innovation Day

Innovation Day is a global observance that celebrates the spirit of creativity, ingenuity, and forward-thinking that drives progress and prosperity in societies around the world. It serves as a reminder of the importance of innovation in driving positive change, fostering economic growth, and addressing pressing challenges facing humanity.

Ways to Celebrate Innovation Day

- Host Innovation Workshops: Organize workshops or brainstorming sessions to encourage creativity and collaboration among team members. Provide opportunities for participants to share ideas, explore new concepts, and develop innovative solutions to real-world problems.

- Showcase Innovative Projects: Highlight innovative projects and initiatives within your organization or community. Share success stories, case studies, and examples of how innovation has made a positive impact on business outcomes, customer satisfaction, or community development.

- Recognize Innovation Champions: Acknowledge individuals or teams who have demonstrated exceptional creativity, leadership, and problem-solving skills. Celebrate their contributions to innovation and inspire others to follow their example.

- Promote Knowledge Sharing: Foster a culture of knowledge sharing and continuous learning by organizing seminars, webinars, or panel discussions on topics related to innovation, technology trends, and emerging markets. Encourage employees to share insights, lessons learned, and best practices with their peers.

- Encourage Experimentation: Create a safe and supportive environment for experimentation and risk-taking. Encourage employees to explore new ideas, test hypotheses, and learn from failures. Embrace a growth mindset that values learning and adaptation as essential components of the innovation process.

Innovation Day serves as a valuable opportunity to celebrate achievements, inspire creativity, and foster a culture of innovation within organizations and communities. By embracing the spirit of innovation and embracing new ideas, organizations can drive positive change, unlock new opportunities, and shape a brighter future for all.

Innovation Fellowship

Innovation fellowships are prestigious programs designed to nurture and support emerging leaders, innovators, and change-makers across various fields and industries. These fellowships provide talented individuals with unique opportunities for professional development, mentorship, and networking, enabling them to drive meaningful innovation, tackle complex challenges, and effect positive change within their organizations and communities. By fostering a culture of innovation and leadership excellence, innovation fellowships contribute to building a diverse pipeline of visionary leaders equipped to shape the future and address pressing global issues.

ey Components of Innovation Fellowships

- Structured Learning Experiences: Innovation fellowships typically offer structured learning experiences, such as workshops, seminars, and training sessions, focused on developing critical skills in innovation, leadership, entrepreneurship, and problem-solving. These learning opportunities equip fellows with the knowledge, tools, and frameworks needed to drive innovation and lead change in their respective fields.

- Mentorship and Coaching: Fellows often receive mentorship and coaching from experienced leaders, industry experts, and seasoned innovators who provide guidance, feedback, and support throughout the fellowship journey. Mentorship relationships help fellows navigate challenges, capitalize on opportunities, and unlock their full potential as innovative leaders.

- Project-Based Assignments: Many innovation fellowships include project-based assignments or innovation challenges where fellows collaborate on real-world problems, develop innovative solutions, and implement initiatives that address societal, environmental, or organizational challenges. These hands-on experiences allow fellows to apply their skills, creativity, and expertise to make tangible impact and drive meaningful change.

- Networking and Collaboration: Innovation fellowships provide fellows with opportunities to connect, collaborate, and build relationships with a diverse community of peers, mentors, and industry leaders. Networking events, conferences, and community-building activities facilitate knowledge sharing, idea exchange, and collaboration, fostering a supportive ecosystem for innovation and learning.

- Access to Resources and Funding: Fellows may gain access to resources, funding, and support services to advance their innovative projects or ventures. Innovation fellowships often provide seed funding, grants, or access to incubators and accelerators to help fellows turn their ideas into actionable projects or scalable ventures with real-world impact.

Innovation fellowships play a crucial role in cultivating a new generation of visionary leaders, innovators, and changemakers who are equipped to tackle complex challenges, drive innovation, and create positive social and economic impact. By investing in talent development, leadership capacity, and cross-sector collaboration, innovation fellowships contribute to building resilient, inclusive, and sustainable communities and organizations poised to thrive in an ever-changing world.

Innovation for Automation

Innovation for automation is a crucial aspect of modernization and efficiency across various industries. Automation involves the use of technology to perform tasks with minimal human intervention, streamlining processes, reducing errors, and enhancing productivity. From manufacturing and logistics to healthcare and finance, automation innovations revolutionize how work is done, leading to cost savings, improved quality, and increased competitiveness.

Benefits of Innovation for Automation

- Increased Efficiency: Automation streamlines repetitive tasks, such as data entry, production line assembly, or customer service inquiries, allowing organizations to allocate human resources to more strategic and value-added activities. For instance, Zapier enhances efficiency by automating workflows between different apps and services, reducing the need for manual oversight in processes like data entry and content management.

- Cost Reduction: By automating routine tasks, organizations can reduce labor costs, minimize errors, and optimize resource utilization, leading to significant cost savings over time. UiPath exemplifies this through its Robotic Process Automation (RPA) capabilities, automating tasks such as invoice processing and email sorting, which significantly lowers operational expenses.

- Improved Accuracy and Quality: Automated systems perform tasks consistently and with precision, minimizing human errors and variability in outputs, thereby enhancing product quality and customer satisfaction. Blue Prism, a Robotic Process Automation (RPA) tool, ensures tasks are executed with high precision and consistency, improving the quality of data management and customer service operations.

- Enhanced Safety: Automation eliminates the need for human workers to perform dangerous or physically demanding tasks, reducing the risk of workplace accidents and injuries. Sarcos Robotics develops robots and exoskeletons that take over hazardous tasks (such as lifting heavy materials, performing high-altitude installations, and handling hazardous substances) in industries like construction, improving safety by protecting employees from potential dangers.

- Scalability: Automated processes can be easily scaled up or down to accommodate fluctuations in demand or business growth, allowing organizations to adapt quickly to changing market conditions. Autodesk Fusion 360 offers a clear example with its cloud-based 3D modeling and manufacturing tools that allow businesses to effortlessly scale their design and production processes in response to market demands or expansion opportunities.

Innovation for automation encompasses a wide range of technologies, including robotics, artificial intelligence, machine learning, and internet of things (IoT) devices. From self-driving cars and smart factories to chatbots and virtual assistants, automation innovations continue to transform industries and redefine the future of work. By embracing innovation for automation, organizations can unlock new opportunities for efficiency, productivity, and growth in the digital age.

Innovation Fund

Innovation funds are financial instruments designed to support and catalyze innovation across various sectors, including technology, healthcare, energy, and agriculture. These funds provide capital to innovative start-ups, research projects, and initiatives with the potential to develop groundbreaking solutions, disrupt industries, and address pressing challenges. By allocating resources to high-potential ventures and ideas, innovation funds play a crucial role in driving economic growth, fostering entrepreneurship, and accelerating the pace of innovation.

Key Components of Innovation Funds

- Venture Capital Investments: Many innovation funds operate as venture capital firms that invest in early-stage and growth-stage start-ups with innovative business models, products, or technologies. These investments typically involve equity financing, where the fund provides capital in exchange for ownership stakes in the companies it supports. Examples of prominent innovation-focused venture capital firms include Andreessen Horowitz, Sequoia Capital, and Accel Partners.

- Corporate Innovation Funds: Corporations and large companies often establish innovation funds to invest in external start-ups, technologies, or research projects that align with their strategic priorities and growth objectives. These corporate innovation funds may operate independently or as part of corporate venture capital (CVC) arms dedicated to sourcing and funding innovative ventures that can enhance the company's competitiveness and drive future innovation.

- Government Grants and Incentives: Governments and public agencies may establish innovation funds to provide grants, subsidies, or tax incentives to support research and development (R&D) activities, technology commercialization, and innovation-driven projects. These funds aim to stimulate innovation across key industries, promote collaboration between academia and industry, and enhance the overall competitiveness of the economy.

- Public-Private Partnerships: Some innovation funds operate as public-private partnerships (PPPs), leveraging combined resources from government entities, private investors, and philanthropic organizations to support innovation initiatives with social or environmental impact. These collaborative efforts pool financial, technical, and intellectual resources to address complex challenges, drive inclusive growth, and achieve sustainable development goals.

- Specialized Innovation Funds: Certain innovation funds focus on specific sectors, technologies, or impact areas, such as clean energy, healthcare innovation, social entrepreneurship, or emerging markets. These specialized funds tailor their investment strategies and criteria to target opportunities that align with their thematic focus areas, leveraging domain expertise and networks to drive sector-specific innovation and impact.

Innovation funds play a pivotal role in fueling the innovation ecosystem by providing capital, mentorship, and strategic support to entrepreneurs, researchers, and innovators. By investing in high-potential ventures and initiatives, these funds help accelerate the development and adoption of transformative solutions that address global challenges, drive economic growth, and create positive social and environmental impact.

Innovation Hub

Innovation hubs are collaborative spaces designed to foster creativity, entrepreneurship, and knowledge-sharing among individuals and organizations. These hubs serve as incubators for innovative ideas and startups, providing access to resources, mentorship, and networking opportunities to support their growth and development.

Benefits of Innovation Hubs

- Cross-Sector Collaboration: Innovation hubs bring together stakeholders from various industries, including technology, healthcare, and finance, facilitating interdisciplinary collaboration and the exchange of ideas. For example, the Cambridge Innovation Center (CIC) in the United States provides shared office spaces and resources for startups and established companies alike, fostering collaboration and innovation across different sectors.

- Access to Resources: Innovation hubs offer access to essential resources such as funding, mentorship, and technical expertise, helping startups overcome common barriers to entry and accelerate their growth. The Nairobi Innovation Week (NIW) in Kenya provides a platform for entrepreneurs to showcase their innovations, connect with investors, and access funding opportunities to scale their ventures.

- Community Building: By providing a supportive and dynamic community of innovators, entrepreneurs, and experts, innovation hubs create an environment conducive to idea generation, experimentation, and learning. The Impact Hub network, with locations worldwide, offers co-working spaces, events, and programs designed to connect social entrepreneurs and drive positive social and environmental change.

- Knowledge Sharing: Innovation hubs serve as hubs of knowledge exchange, offering workshops, seminars, and networking events where members can learn from industry leaders, share best practices, and gain insights into emerging trends and technologies. The Innovation Factory in Belfast, Northern Ireland, hosts regular events and training programs to support startups and SMEs in developing their innovative ideas and business skills.

- Catalyst for Economic Growth: By fostering innovation and entrepreneurship, innovation hubs contribute to economic growth and job creation in their local communities. The Cape Innovation and Technology Initiative (CiTi) in South Africa, for instance, has played a significant role in transforming Cape Town into a thriving tech ecosystem, attracting investment and talent to the region.

In summary, innovation hubs play a vital role in driving innovation, economic growth, and social impact by providing a supportive ecosystem where ideas can flourish, startups can thrive, and communities can prosper. Whether they are physical spaces, virtual platforms, or collaborative networks, these hubs serve as catalysts for positive change and progress.

Innovation Lab

Innovation labs serve as creative spaces within organizations dedicated to fostering innovation, experimentation, and collaboration. These labs provide a structured environment for teams to ideate, prototype, and test new ideas and technologies, driving organizational growth and competitiveness. From tech giants to startups and government agencies, innovation labs play a vital role in driving breakthrough innovations and shaping the future of various industries.

Key Components of Innovation Labs

- Cross-functional Teams: Innovation labs bring together diverse teams comprising experts from different disciplines, including designers, engineers, marketers, and business strategists, to foster interdisciplinary collaboration and creativity.

- Design Thinking Methodology: Labs often employ design thinking methodologies to approach problem-solving and innovation systematically, focusing on understanding user needs, ideating solutions, prototyping concepts, and iterating based on feedback.

- Prototyping Facilities: Innovation labs are equipped with state-of-the-art prototyping tools and facilities, including 3D printers, CNC machines, and electronics labs, allowing teams to quickly iterate and test physical prototypes of their ideas.

- Agile Framework: Labs operate within agile frameworks, enabling teams to work iteratively, adapt to changing requirements, and deliver tangible results quickly. Agile principles such as sprints, stand-up meetings, and retrospectives facilitate rapid experimentation and learning.

- Collaboration Spaces: Innovation labs feature collaborative workspaces designed to inspire creativity and foster communication among team members. These spaces may include open-plan offices, brainstorming rooms, and breakout areas conducive to idea generation and knowledge sharing.

Case Study: Microsoft AI Co-Innovation Lab

Case Study: Microsoft AI Co-Innovation Lab- Company: Microsoft

- Innovation Lab: AI Co-Innovation Lab, 555 California Street, USA (launched Sep-2023)

- What Was Done: Microsoft unveiled its fifth AI Co-Innovation Lab, nestled in the bustling heart of downtown San Francisco. This new establishment aims to serve as a beacon for AI development, offering unparalleled access to AI expertise, cutting-edge tools, and robust infrastructure. The lab is designed to foster a collaborative environment for startups and enterprises alike, facilitating the development and testing of AI prototypes and solutions. Emphasizing the strategic placement of the lab, Microsoft recognizes San Francisco's pivotal role in AI innovation, especially within the startup ecosystem. The initiative underlines Microsoft's commitment to democratizing AI technology, enabling entities ranging from fledgling startups to large enterprises to harness the transformative power of AI.

- Results/Impact: The AI Co-Innovation Lab has quickly become a cornerstone for AI advancement in San Francisco. By providing a platform for ideation and prototyping, the lab has significantly accelerated the AI development lifecycle for many participating companies. A testament to the lab's success is the collaboration with the startup Space and Time. Through the lab's support, Space and Time harnessed Microsoft's SQL Server technology, integrating it with Web3 data and employing generative AI to simplify complex SQL queries. This breakthrough exemplifies the lab's impact, showcasing how access to advanced AI resources and expertise can revolutionize data processing and analysis. As Microsoft continues to invest in AI and cybersecurity startups through its M12 Venture Fund, the AI Co-Innovation Lab stands as a vital resource for innovators seeking to explore the frontiers of AI technology and its applications.

Innovation labs have emerged as hotbeds of creativity and innovation, driving breakthroughs in technology, product development, and customer experience. By providing a supportive environment for experimentation and risk-taking, these labs empower organizations to stay ahead of the curve and address emerging challenges in an ever-changing market landscape.

Innovation Leader

Innovation leadership is a critical aspect of driving forward progress and change within organizations. An effective innovation leader not only fosters a culture of creativity and experimentation but also provides strategic direction and resources to support innovative initiatives.

Following is a closer look at the role of innovation leaders and what sets them apart.

Visionary Guidance

- An innovation leader sets a clear vision for the organization's innovation goals and priorities, aligning them with the overall business strategy.

- For example, Sara Blakely, the founder of Spanx, demonstrated innovation leadership by identified a gap in the market for comfortable, flattering undergarments that were invisible under clothing, and envisioning and creating a revolutionary product , which `transformed the fashion industry with her innovative approach to shapewear. Her use of breathable, lightweight fabrics and seamless designs that eliminated visible lines transformed the industry's approach to undergarments, making Spanx a pioneering brand in fashion innovation.

Encouraging Creativity

- Innovation leaders cultivate a supportive environment where employees feel empowered to explore new ideas and take calculated risks.

- Take Pixar's Ed Catmull, for instance, who fostered a culture of creativity and collaboration, leading to groundbreaking animated films like "Toy Story" and "Finding Nemo."

Championing Experimentation

- They encourage experimentation and provide resources for research and development, allowing for the exploration of innovative solutions.

- At Google's X Lab, led by Astro Teller, moonshot projects like Google Glass and Project Loon were pursued, pushing the boundaries of innovation through ambitious experimentation.

Embracing Diversity

- Effective innovation leaders value diversity of thought and encourage diverse perspectives to drive innovation.

- IBM's Ginni Rometty promoted diversity and inclusion within the company, fostering innovation by leveraging the unique strengths and perspectives of employees from different backgrounds.

Adapting to Change

- They adapt to change and navigate uncertainty with resilience, continuously seeking new opportunities for innovation.

- Satya Nadella, CEO of Microsoft, embraced a growth mindset and led the company's transformation by shifting its focus towards cloud computing and AI-driven innovations.

In conclusion, innovation leaders play a pivotal role in shaping the future of organizations by fostering a culture of innovation, empowering teams to push boundaries, and driving strategic initiatives that lead to impactful outcomes. By embodying visionary leadership qualities and embracing the principles of creativity and experimentation, they pave the way for transformative innovation and sustainable growth.

Innovation Network

An innovation network refers to a collaborative ecosystem of individuals, organizations, and resources focused on driving innovation and fostering growth in various industries. These networks facilitate knowledge sharing, partnership building, and resource mobilization, accelerating the pace of innovation and addressing complex challenges more effectively. From industry-specific consortia to global innovation hubs, innovation networks play a crucial role in fostering cross-sector collaboration and driving collective impact.

Key Elements of Innovation Networks

- Cross-Sector Collaboration: Innovation networks bring together stakeholders from diverse sectors, including academia, government, industry, and non-profit organizations, to exchange ideas, expertise, and resources. This interdisciplinary approach promotes cross-pollination of ideas and facilitates the emergence of novel solutions to complex problems.

- Open Innovation Platforms: Many innovation networks leverage open innovation platforms and digital collaboration tools to connect participants and facilitate collaboration in real-time. These platforms enable crowdsourcing of ideas, co-creation of solutions, and rapid iteration, accelerating the innovation process and driving collective intelligence.

- Incubators and Accelerators: Innovation networks often include incubators, accelerators, and startup hubs that provide support services, mentorship, and funding to early-stage ventures. These programs help nurture entrepreneurial talent, catalyze technology commercialization, and accelerate the growth of innovative startups.

- Knowledge Exchange Initiatives: Innovation networks organize events, workshops, and conferences to facilitate knowledge exchange, capacity building, and networking opportunities among members. These initiatives foster a culture of learning and collaboration, enabling participants to stay abreast of the latest trends, best practices, and emerging technologies.

- Collaborative Projects and Initiatives: Innovation networks drive collaborative projects and initiatives aimed at addressing shared challenges and achieving common goals. These initiatives may involve joint research and development efforts, technology pilots, or industry-wide standards-setting activities, leveraging the collective expertise and resources of network participants.

Innovation networks are instrumental in driving systemic change, fostering resilience, and unlocking new opportunities for growth and development. By harnessing the collective wisdom and creativity of diverse stakeholders, these networks catalyze innovation ecosystems and drive positive change at local, regional, and global levels.

Innovation to Zero

"Innovation to Zero" refers to the ambitious goal of achieving zero emissions, waste, or other negative impacts through innovative solutions and practices. This concept has gained traction in various sectors, including energy, transportation, and manufacturing, as organizations strive to minimize their environmental footprint and contribute to a more sustainable future.

Following is a closer look at innovation to zero and its implications.

Zero Emissions

- Innovative technologies and practices aim to eliminate or significantly reduce greenhouse gas emissions, such as carbon dioxide, methane, and nitrous oxide, to combat climate change.

- For example, Tesla's electric vehicles and solar energy solutions contribute to reducing carbon emissions from transportation and electricity generation, advancing the transition to a low-carbon economy.

Zero Waste

- Innovations in waste management and resource efficiency aim to minimize waste generation and maximize recycling and reuse of materials.

- Loop, a circular shopping platform, partners with leading brands to offer products in reusable packaging, eliminating single-use packaging waste and promoting a zero-waste lifestyle.

Zero Harm

- Organizations strive to eliminate harm to people, communities, and the environment through innovative safety measures and risk mitigation strategies.

- In the oil and gas industry, companies like Shell have implemented innovative technologies and practices to enhance safety and prevent environmental incidents, such as oil spills and leaks.

Zero Deforestation

- Innovative solutions aim to halt deforestation and promote sustainable land use practices, preserving biodiversity and ecosystem services.

- The Rainforest Alliance's innovative certification programs and supply chain initiatives help companies adopt responsible sourcing practices, reducing deforestation and promoting forest conservation.

Zero Poverty

- Innovative approaches to economic development and social inclusion aim to eradicate poverty and promote shared prosperity.

- Microfinance institutions like Grameen Bank leverage innovative financial tools and services to provide access to credit and empower marginalized communities, lifting them out of poverty.

In conclusion, innovation to zero represents a bold and ambitious vision for creating a more sustainable and equitable world. By harnessing the power of innovation, organizations and individuals can work together to address pressing global challenges and achieve meaningful progress towards zero emissions, waste, harm, deforestation, and poverty.

Innovation Value

Understanding the value of innovation is essential for organizations seeking to remain competitive and relevant in today's rapidly evolving business landscape. Innovation adds value in various ways, driving growth, efficiency, and differentiation.

Following is a closer look at the value of innovation and how it impacts organizations.

Driving Growth

- Innovation fuels growth by creating new products, services, and business models that meet evolving customer needs and preferences.

- For example, Airbnb disrupted the hospitality industry by introducing a platform that connects travelers with unique accommodations, driving growth by tapping into the sharing economy.

Enhancing Efficiency

- Innovative technologies and processes streamline operations, reduce costs, and improve productivity, leading to greater efficiency.

- Tesla's innovative approach to manufacturing electric vehicles, such as its Gigafactories and automated production lines, has enabled the company to achieve higher levels of efficiency and scalability.

Differentiating from Competitors

- Innovation allows organizations to differentiate themselves from competitors by offering unique value propositions and experiences.

- Apple's innovative product design, user interface, and ecosystem have set it apart in the competitive tech industry, driving customer loyalty and market leadership.

Solving Complex Challenges

- Innovative solutions address complex challenges and opportunities, ranging from environmental sustainability to healthcare and social issues.

- The Ocean Cleanup, founded by Boyan Slat, developed innovative technologies to remove plastic pollution from the world's oceans, addressing a pressing global environmental challenge.

Creating Value for Stakeholders

- Innovation generates value for stakeholders, including customers, employees, investors, and communities, by delivering tangible benefits and positive outcomes.

- Patagonia's commitment to sustainable and ethical practices, along with innovative initiatives like its Worn Wear program, creates value for customers, employees, and the environment, fostering brand loyalty and social impact.

In conclusion, the value of innovation extends far beyond product development and revenue generation. It drives growth, efficiency, differentiation, and social impact, positioning organizations for long-term success and sustainability. By recognizing and leveraging the value of innovation, organizations can stay ahead of the curve and thrive in an increasingly competitive and dynamic business environment.

Innovation without Limits

Innovation without limits signifies a mindset and approach that transcends traditional boundaries and constraints, enabling individuals and organizations to unleash their full creative potential and drive meaningful change. This concept emphasizes the importance of fostering a culture of innovation that embraces experimentation, risk-taking, and continuous learning, regardless of existing limitations or challenges. By adopting an open-minded and forward-thinking mindset, individuals and organizations can overcome barriers, explore new possibilities, and pioneer groundbreaking innovations that have the power to transform industries and society.

Unlocking Innovation Without Limits

- Embrace Diversity and Inclusion: Creating diverse and inclusive environments fosters a broader range of perspectives, ideas, and experiences, fueling creativity and innovation. By embracing diversity in backgrounds, skills, and perspectives, organizations can tap into a wealth of untapped potential and drive innovation without limits.

- Empowerment and Autonomy: Providing individuals with the autonomy and freedom to explore new ideas, experiment with different approaches, and take calculated risks is essential for fostering innovation without limits. Empowered employees are more likely to think creatively, challenge the status quo, and drive meaningful change within their organizations.

- Cultivate a Growth Mindset: Cultivating a growth mindset, characterized by a belief in one's ability to learn and grow, is essential for fostering innovation without limits. Encouraging a culture of continuous learning, resilience, and adaptability enables individuals to overcome setbacks, embrace failure as a learning opportunity, and push the boundaries of what is possible.

- Remove Silos and Barriers: Breaking down organizational silos and removing bureaucratic barriers is crucial for fostering collaboration, communication, and knowledge sharing across departments and disciplines. By creating open, transparent, and interconnected work environments, organizations can facilitate cross-pollination of ideas, accelerate innovation, and unleash creativity without limits.

- Invest in Innovation Infrastructure: Providing access to resources, tools, and technologies that support innovation is essential for enabling individuals and teams to bring their ideas to life. Whether it's investing in state-of-the-art facilities, digital collaboration platforms, or innovation labs, organizations must prioritize building the necessary infrastructure to support innovation without limits.

Innovation without limits empowers individuals and organizations to push the boundaries of what is possible, challenge conventional thinking, and drive transformative change. By fostering a culture of creativity, collaboration, and experimentation, organizations can unlock new opportunities, drive competitive advantage, and shape the future of their industries.

Intellectual Properties (IP)

Intellectual properties (IP) encompass a range of intangible assets, including patents, trademarks, copyrights, and trade secrets, which play a crucial role in protecting and monetizing innovation. These legal protections provide innovators with exclusive rights to their creations, enabling them to commercialize their ideas, secure competitive advantage, and drive value for their businesses. Understanding the intricacies of intellectual property law and strategically managing IP assets is essential for safeguarding innovation and maximizing its impact in today's knowledge-based economy.

Navigating Intellectual Properties

- Patents: Patents grant inventors exclusive rights to their inventions, preventing others from making, using, or selling the patented technology without permission. By securing patents for novel and non-obvious inventions, innovators can protect their technological advancements and deter competitors from copying their ideas.

- Trademarks: Trademarks are symbols, names, or phrases used to distinguish goods or services from those of competitors. Registering trademarks helps businesses build brand recognition, establish goodwill with customers, and prevent others from using similar marks that could cause confusion in the marketplace.

- Copyrights: Copyrights protect original works of authorship, including literary, artistic, and musical creations, by granting creators exclusive rights to reproduce, distribute, and display their works. Registering copyrights provides creators with legal recourse against infringement and enables them to monetize their creative endeavors through licensing and royalties.

- Trade Secrets: Trade secrets consist of confidential information, such as formulas, processes, or customer lists, which derive economic value from not being generally known or readily ascertainable. Protecting trade secrets requires implementing robust security measures, such as non-disclosure agreements and access controls, to prevent unauthorized access or disclosure.

- Enforcement and Litigation: Enforcing intellectual property rights often involves litigation or other legal proceedings to address infringement or misappropriation by third parties. Partnering with experienced IP attorneys and leveraging legal remedies, such as injunctions and damages awards, can help protect innovators' interests and deter intellectual property violations.

Effective management of intellectual properties is essential for preserving innovation, fostering economic growth, and driving competitive advantage in today's global marketplace. By strategically leveraging patents, trademarks, copyrights, and trade secrets, innovators can protect their valuable creations, attract investment, and capitalize on their innovative ideas to achieve long-term success.

Radical Innovation

Radical innovation represents a significant departure from existing technologies, products, or business models, often leading to transformative changes in industries and society. Unlike incremental improvements, radical innovations introduce groundbreaking ideas that revolutionize the way we live, work, and interact. Embracing radical innovation requires a willingness to challenge the status quo, disrupt established norms, and pursue ambitious goals that push the boundaries of what is possible.

Embracing Radical Innovation

- Disruptive Technologies: Radical innovations often emerge from disruptive technologies that fundamentally change the way industries operate. Examples include blockchain technology, which has the potential to revolutionize finance, supply chain management, cybersecurity, and gene editing techniques like CRISPR-Cas9, which hold promise for curing genetic diseases and transforming healthcare.

- Transformative Business Models: Radical innovation extends beyond technological advancements to encompass novel business models that redefine industry dynamics. Companies like Airbnb and Uber have disrupted traditional hospitality and transportation industries by leveraging digital platforms to connect consumers with underutilized resources, such as spare rooms and vehicles, creating entirely new markets in the process.

- Cross-Disciplinary Collaboration: Radical innovation often requires collaboration across diverse disciplines, bringing together experts from different fields to tackle complex challenges. Initiatives like interdisciplinary research hubs and innovation labs facilitate knowledge exchange, creative problem-solving, and the cross-pollination of ideas, driving breakthrough innovations that transcend traditional boundaries.

- Further reading: How to Gather Extreme Ideas

- Risk-Taking and Experimentation: Embracing radical innovation requires a willingness to take risks, experiment with unconventional ideas, and embrace failure as an inherent part of the innovation process. Organizations that cultivate a culture of experimentation and learning foster an environment where radical ideas can flourish, leading to disruptive innovations that reshape industries and create new opportunities.

- Long-Term Vision and Persistence: Achieving radical innovation often requires a long-term vision and unwavering persistence in the face of challenges and setbacks. Innovators who remain committed to their bold ideas, despite initial skepticism or resistance, can overcome obstacles and drive meaningful change that has a lasting impact on society.

- Further reading: How to Deal with Extreme Ideas

By embracing radical innovation, organizations can unlock new sources of value, drive sustainable growth, and position themselves as leaders in their respective industries. Whether through disruptive technologies, transformative business models, or cross-disciplinary collaboration, radical innovation holds the potential to catalyze positive change and shape the future in profound and unexpected ways.

Thinking Tools

Thinking tools are essential aids for fostering creativity, problem-solving, and innovation in various fields. These tools provide structured frameworks and methods to generate ideas, analyze problems, and make informed decisions. Incorporating thinking tools into the innovation process can enhance productivity, collaboration, and outcomes by enabling individuals and teams to approach challenges systematically and strategically.

Following are some examples of thinking tools and their applications.

Mind Mapping

- Mind mapping is a visual brainstorming technique that helps organize thoughts and ideas around a central theme or concept.

- Example: MindMeister is a web-based mind mapping tool that allows users to create, share, and collaborate on mind maps in real-time.

SWOT Analysis

- SWOT analysis is a strategic planning tool used to identify strengths, weaknesses, opportunities, and threats related to a project, product, or organization.

- Example: Trello, a project management tool, offers built-in templates for conducting SWOT analyses and other strategic planning activities.

Six Thinking Hats

- Six Thinking Hats is a method developed by Edward de Bono for exploring different perspectives on a problem or decision.

- Example: Miro, an online collaborative whiteboard platform, provides templates and tools for implementing the Six Thinking Hats technique in virtual brainstorming sessions

Design Thinking

- Design thinking is a human-centered approach to innovation that emphasizes empathy, ideation, prototyping, and testing.

- Example: Figma is a design collaboration tool that supports the design thinking process by enabling teams to create, iterate, and share interactive prototypes.

Force Field Analysis

- Force Field Analysis is a technique for examining the driving and restraining forces influencing a desired change or outcome.

- Example: Lucidchart is a diagramming tool that offers features for creating force field analysis diagrams and visualizing the factors impacting decision-making.

Systematic Inventive Thinking (SIT)

- SIT is a method that encourages constraints in thinking, which paradoxically leads to greater creativity—a key entrepreneurship skill.

- Gilad Fisker, for example, employed SIT principles in developing Fisker Automotive's hybrid electric vehicles, which challenge conventional automotive design and reflect a sustainable approach to transportation.

- Further Reading: The Six Thinking Tools for Predicting New Products

Incorporating these thinking tools into the innovation process can help individuals and teams generate creative solutions, identify opportunities, and overcome obstacles more effectively. By leveraging the power of structured thinking, organizations can foster a culture of innovation and drive meaningful change in their respective industries.

Innovation Glossary - 200 Terms

Here you will find 200 Innovation term definitions and explanations. These terms cover almost every aspect of innovation.

If you want to finds out more about any of these terms terms you can click on the links suggesting futher reading (many of the terms have full articles about them in our website), or search for further details about this these terms here.

You can also suggest additional terms to add to this gloassary, by contacting us here.

We hope you will find this gloassary useful, and wish you a succesful and innovative day!

- Absorptive Capacity: This term refers to a company's ability to recognize valuable external information, assimilate it, and apply it to commercial ends. It is critical in innovation as it determines how effectively a business can leverage external knowledge to advance its own technology and practices.

- Agile Development: A methodology primarily used in software development where requirements and solutions evolve through the collaborative effort of self-organizing and cross-functional teams. It advocates adaptive planning, evolutionary development, early delivery, and continual improvement, and it encourages flexible responses to change. Read More

- Angel Investor: An individual who provides capital for a business start-up, usually in exchange for convertible debt or ownership equity. Angel investors are often found among an entrepreneur's family and friends and are willing to invest in the early stages of a business.

- Augmented Reality (AR): A technology that superimposes a computer-generated image on a user's view of the real world, thus providing a composite view. AR enhances users' perception of reality by overlaying digital information on live camera feeds, unlike virtual reality, which replaces the real world with a simulated one.

- Automation: The use of various control systems for operating equipment such as machinery, processes in factories, boilers, and heat treating ovens, with minimal or reduced human intervention. Automation is widely used to improve productivity, quality, and consistency in manufacturing and other sectors. Read about automation of Innovation Processes.

- Balanced Scorecard: A strategic planning and management system used extensively in business and industry, government, and nonprofit organizations worldwide to align business activities to the vision and strategy of the organization, improve internal and external communications, and monitor organizational performance against strategic goals.

- Benchmarking: The process of comparing one's business processes and performance metrics to industry bests or best practices from other industries. Dimensions typically measured are quality, time, and cost. Benchmarking is used to measure performance using a specific indicator resulting in a metric of performance that is then compared to others.

- Beta Testing: A type of testing period for a computer product prior to any sort of commercial or official release. Beta testing is considered the last stage of testing, and it involves distributing the product to beta test users for real-world exposure. Other pre-release tests typically do not involve actual customers.

- Big Data: Refers to extremely large data sets that may be analyzed computationally to reveal patterns, trends, and associations, especially relating to human behavior and interactions. Much of big data comes from data mining and has the potential to help companies improve operations and make faster, more intelligent decisions.

- Blue Ocean Strategy: A marketing theory and the title of a book published in 2004 that suggests companies are better off searching for ways to gain "uncontested market space" rather than competing with similar companies. The concept aims to make the competition irrelevant by creating a leap in value for both the company and its customers. Read about Blue Oceans in Israel.

- Bootstrapping: This approach refers to building a company from the ground up with nothing but personal savings, and the cash coming in from initial sales. Companies that bootstrap their way through initial founding are often more sustainable and grounded as they do not rely on external funding.

- Brainstorming: A group creativity technique designed to generate a large number of ideas for the solution of a problem. During the session, participants are encouraged to come up with thoughts and ideas that can at first seem to be a bit off the mark. Ideas are not criticized and participants work together to develop or combine them into the best solutions. Read More.

- Brand Equity: The value a company gains from a product with a recognizable and admired name when compared to a generic equivalent. Brand equity is built on a strong reputation and consistent consumer satisfaction. It can result in differential pricing, customer loyalty, and a stronger competitive position.

- Breakthrough Innovation: This type of innovation refers to radical, disruptive changes in products or processes that transform existing markets or create new ones. Breakthroughs can redefine the standards of products and services, and often deliver significant new value to the customer.

- Business Incubator: An organization designed to accelerate the growth and success of entrepreneurial companies through an array of business support resources and services that could include physical space, capital, coaching, common services, and networking connections.

- Business Model Canvas: A strategic management template used for developing new business models and documenting existing ones. It offers a visual chart with elements describing a firm's or product's value proposition, infrastructure, customers, and finances, assisting businesses in aligning their activities by illustrating potential trade-offs. Read more.

- Business Model Innovation: Refers to the creation, or reinvention, of a business itself, as opposed to products or services. The strategy focuses on delivering new value to customers, tapping into new markets, and changing the dynamics of an existing sector.

- Business Process Reengineering: A business management strategy focusing on the analysis and design of workflows and business processes within an organization. BPR aims to help organizations fundamentally rethink how they do their work in order to dramatically improve customer service, cut operational costs, and become world-class competitors.

- Business Strategy: Long-term planning of a business's overall direction. A business strategy is typically defined as a set of competitive moves and actions that business uses to attract customers, compete successfully, strengthening performance, and achieve organizational goals.Read about the difference between business strategy and marketing strategy.

- Capability Maturity Model: A development model created after study of data collected from organizations that contracted with the U.S. Department of Defense, which describes the maturity of an organization's software development processes. It is widely used in software engineering to describe how well an organization’s processes allow them to produce and maintain quality software.

- Capital Raising: The process of sourcing financial support for business ventures, typically done through venture capital investments, angel investments, or public and private offerings. This is crucial for startups and established businesses aiming to expand operations, enter new markets, or develop new products.

- Change Management: The approach to transitioning individuals, teams, and organizations to a desired future state. In business, effective change management goes beyond simple management tasks to include leadership and the strategic alignment of the company's culture, values, people, and behaviors to realize change.

- Chief Innovation Officer: A position in a company tasked with managing the innovation process within the organization, aligning the company's strategy with innovation opportunities. The role often involves fostering a culture of innovation and driving creative problem-solving at all levels of the organization. Read more.

- Co-creation: A business strategy focusing on customer experience and interactive relationships. Co-creation allows and encourages a more active involvement from customers to create a value rich experience. This can involve new product development, enhancements, and customization.

- Commercialization: The process of bringing new products or services to market. It encompasses production, distribution, marketing, sales, and customer support. Commercialization is a critical phase in the business cycle and requires careful planning to ensure product adoption and market penetration. Read More, Also - Read about "Innovation to Market".

- Competitive Advantage: An attribute that allows an organization to outperform its competitors. This advantage can come from access to special resources, a highly skilled workforce, geographic location, high entry barriers, and other factors that contribute to greater sales or lower costs.

- Competitive Intelligence: The action of defining, gathering, analyzing, and distributing intelligence about products, customers, competitors, and any aspect of the environment needed to support executives and managers in strategic decision making for an organization. Read about Competitive Analysis.

- Concept Testing: A process of using qualitative and quantitative methods to evaluate consumer response to a product idea before introducing the product to the market. Concept testing can be used to refine a product concept, target the right audience, and save time and money in product development. Read More,

- Consumer Insights: The interpretation of trends in human behaviors which aims to increase effectiveness of a product or service for the consumer, as well as increase sales for mutual benefit. These insights can be gathered from observing consumers in action or through direct questioning.

- Continuous Improvement: An ongoing effort to improve products, services, or processes over time. These efforts can seek "incremental" improvement over time or "breakthrough" improvement all at once. Techniques common in manufacturing, such as Six Sigma and Kaizen, are used to foster continuous improvement. Read about "Innovation or Improvement?".

- Convergence: In business, the merging of distinct technologies, industries, or devices into a unified whole. This blending creates new opportunities and markets. Technological convergence, for example, refers to the trend where different forms of digital media are combined into a digital form.

- Corporate Entrepreneurship: The practice of a corporate management style that integrates risk-taking and innovation approaches, as well as the reward and motivational techniques that are more traditionally thought of as being the province of entrepreneurship. Read about "Business Innovation".

- Corporate Strategy: A strategy that defines the scope of the business in terms of the industries and markets in which it operates. Corporate strategies involve identifying the business areas in which the company intends to operate, and the development of policies and plans for efficiently deploying the resources required to achieve goals.

- Corporate Venture Capital: A subsidiary of a large firm that makes venture capital investments. By investing in external start-up companies, the large firm seeks to obtain a window on new technologies, gain access to new markets, and ensure a pipeline of future innovations to sustain its corporate growth.

- Creativity: The use of imagination or original ideas to create something; in business, creativity involves generating ideas that result in the improved efficiency or effectiveness of a system or process. Read about "Are Innovation and Creativity the same?"

- Crowdfunding: A method of raising capital through the collective effort of friends, family, customers, and individual investors. This approach taps into the collective efforts of a large pool of individuals—primarily online via social media and crowdfunding platforms—and leverages their networks for greater reach and exposure.

- Crowdsourcing: The practice of obtaining needed services, ideas, or content by soliciting contributions from a large group of people, and especially from an online community, rather than from traditional employees or suppliers.

- Customer Development: A methodology for building startups and new corporate ventures. It is one of the three parts that make up a Lean Startup, centering on a hypothesis-driven approach to understanding who the customers are, what problems they need to solve, and what solution they will willingly pay for.

- Customer Experience: Encompasses every aspect of a company’s offering—the quality of customer care, of course, but also advertising, packaging, product and service features, ease of use, and reliability. Creating a good customer experience is seen as a key way to differentiate a company from its competitors.

- Data Analytics: The science of analyzing raw data to make conclusions about that information. Data analytics techniques enable companies to make more-informed business decisions and many, often in real-time, use sophisticated analytics tools and software capabilities. Read More.

- Data Mining: The process of discovering patterns and relationships in large volumes of data by using statistical techniques and software. Data mining is used across a variety of fields, including marketing, medicine, and research, to make predictions and decisions based on the analysis of data. Read about "Innovation with Data".

- Design Thinking: A non-linear, iterative process that teams use to understand users, challenge assumptions, redefine problems, and create innovative solutions to prototype and test. It involves five phases—empathize, define, ideate, prototype, and test. This approach is especially useful in tackling complex problems that are ill-defined or unknown. Read More,

- Digital Disruption: The change that occurs when new digital technologies and business models affect the value proposition of existing goods and services. Digital disruption is often the result of startups offering new ways to deliver services more cheaply, conveniently, or effectively.

- Digital Transformation: The integration of digital technology into all areas of a business, fundamentally changing how businesses operate and deliver value to customers. It's also a cultural change that requires organizations to continually challenge the status quo, experiment, and get comfortable with failure.

- Discontinuous Innovation: A term used to describe innovations that make significant changes in how problems are solved, by creating new products or services that do not initially meet the needs of existing customers but may find new markets. These innovations can disrupt or create entire industries.

- Disruptive Innovation: A type of innovation that significantly alters the way that businesses operate. A disruptive innovation is not just a simple improvement but something that causes older technologies or products to become obsolete. The classic example is how smartphones replaced flip phones. Read more.

- Diversification: The strategy of entering into new markets or industries which are not related to the existing business portfolio, thereby spreading risk. Companies may diversify for strategic reasons such as to achieve growth, reduce risk, or capitalize on a firm’s core competencies. Read about "how to develop an umbrella brand".

- Early Adopters: A category of consumers who are first to purchase and use a new product or technology. Early adopters are key to the success of new products, as they help to validate product market fit, provide feedback, and generate word-of-mouth marketing.

- Ecosystem: In business, an ecosystem is a complex network of interconnected organizations that depend on each other for their mutual survival. Examples include technology ecosystems where multiple companies may contribute to the development and delivery of a particular technology.

- Elevator Pitch: A succinct and persuasive sales pitch that outlines the essence of a project, business, or product idea in a way that any listener can understand it in a short period of time. An elevator pitch is typically around 30 seconds, the time it takes for an elevator ride.

- Emerging Technologies: Technologies that are currently developing or will be developed over the next five to ten years, and which will substantially alter the business and social environment. These include advanced robotics, biotechnology, artificial intelligence, and more.

- Empathy Map: A tool used in design thinking and user experience design to gain a deeper insight into customers. It is a visual map that describes a customer's behaviors and attitudes in order to help you understand their experiences and motivations.

- Entrepreneur: An individual who starts and runs a business with limited resources and planning, taking account of all the risks and rewards of their business venture. The entrepreneur is often seen as an innovator—a generator of new ideas, and business processes. Read more.

- Entrepreneurial Finance: The study and practice of financial management in entrepreneurial ventures. It primarily deals with financing, valuation, and investment decisions in new and emerging businesses.

- Entrepreneurship: The activity of setting up a business or businesses, taking on financial risks in the hope of profit. Entrepreneurship is often associated with true uncertainty, particularly when it involves bringing something genuinely novel to the market. Read about "Innovation in Entrepreneurship".

- Entry Barriers: Factors that prevent or hinder companies from entering an industry and competing on an equal basis with established incumbents. These can include high start-up costs, stringent regulations, customer loyalty, and access to suppliers or distribution channels.

- Environmental Scanning: The process by which companies monitor the external macro and microenvironment to understand the environment in which they operate. This can help predict trends and understand the landscape to better make strategic decisions.

- Exponential Organizations: Organizations whose impact or output is disproportionately large—typically more than 10 times larger—compared to its peers because of the use of new organizational techniques that leverage accelerating technologies.

- Forecasting: The process of making predictions of the future based on past and present data and analysis of trends. Forecasting is used in business for planning purposes in areas such as budgeting, sales, marketing, and more. Read about "The next big innovation".

- Frugal Innovation: An approach to developing products and solutions that minimizes the use of financial and material resources in the design and production process. Frugal innovation is especially significant in developing countries, enabling companies to create high-quality products at significantly reduced costs.

- Funding Rounds: Stages through which startups typically raise capital to finance their growth. Common rounds include seed (initial funding), Series A, B, C, and sometimes D or beyond, depending on the company's development stage and needs. Each round involves negotiations concerning valuation, equity, and investment terms.

- Future-proofing: A strategy involving the anticipation of future developments to minimize negative impacts while taking advantage of potential opportunities. Future-proofing is often used in technology sectors by developing products and systems that are adaptable to future technologies and market changes.

- Gamification: The application of game-design elements and game principles in non-game contexts. Gamification techniques strive to leverage people's natural desires for socializing, learning, mastery, competition, achievement, status, and self-expression to achieve greater engagement and loyalty.

- Growth Hacking: A marketing technique developed by startups which uses creativity, analytical thinking, and social metrics to sell products and gain exposure. Growth hacking focuses on low-cost and innovative alternatives to traditional marketing, rapidly testing persuasive copy, email marketing, SEO, and viral strategies.

- Horizon Scanning: A technique for detecting early signs of potentially important developments through a systematic examination of potential threats and opportunities. It is typically used in strategic planning, to anticipate significant changes that lie beyond the organization's current planning horizon.

- Human-Centered Design: An approach to systems design and development, conceived from the point of view of the human user. Human-centered design seeks to make systems usable and useful by focusing on the users, their needs and requirements, and by applying human factors, usability knowledge, and techniques.

- Ideation: The creative process of generating, developing, and communicating new ideas. Ideation encompasses all stages of a thought cycle, from innovation, to development, to actualization. Ideation can be conducted individually or in a group setting. Read More.

- Incremental Innovation: Refers to minor improvements or simple adjustments in current products, services, processes, or methods. The goal is to maintain or improve the competitive position over time. Incremental innovation does not require radical new technology or ideas but instead builds on existing capabilities.

- Industry 4.0: Refers to the new phase in the Industrial Revolution that focuses heavily on interconnectivity, automation, machine learning, and real-time data. Industry 4.0 integrates physical production and operations with smart digital technology, machine learning, and big data to create a more holistic and better connected ecosystem for companies that focus on manufacturing and supply chain management.

- Information Asymmetry: A situation where one party in a transaction has more or superior information compared to another. This often happens in transactions where the seller knows more about the product than the buyer, potentially leading to an imbalance in power during negotiations.

- Innovation Audit: A thorough analysis of the innovation capabilities of a company. An innovation audit examines how effectively an organization is handling its innovation processes and activities, aiming to identify areas where improvements can be made to boost the innovation performance.

- Innovation Champion: An individual within an organization who drives the innovation process by promoting, encouraging, and managing the execution of new ideas. These champions are critical for overcoming resistance to change and for achieving the successful implementation of new business strategies and innovations. Read more.

- Innovation Culture: A work environment that organizations cultivate to nurture unorthodox thinking and its application. Offices with an innovation culture encourage new ideas and innovations. Employees are rewarded for coming up with new ways to improve the business, not just through incentives but also through recognition and support. Read more.

- Innovation Ecosystem: Refers to a network of interconnected entities that mutually support, reinforce, and enhance the growth and profitability of innovative products and services. This includes suppliers, producers, competitors, customers, and regulatory bodies, all functioning within a particular market or geography.

- Innovation Funnel: A visual representation used to guide the innovation process, which is typically segmented into stages (such as idea generation, screening, development, and commercialization). This funnel helps in managing the flow of ideas and determining which ones should be pursued.

- Innovation Management: The discipline of managing processes in innovation. It can be used to develop both product and organizational innovations. Innovation management includes a set of tools that allow managers and engineers to cooperate with a common understanding of processes and goals. Read More.

- Innovation Metrics: Quantitative measures that track how effective companies are at achieving results from their innovation efforts. These metrics can include inputs (like the number of ideas generated) and outputs (such as revenue from new products). Read about "Innovation KPIs".